Abstract and Citation

Zack Cooper, Stuart V. Craig, Aristotelis Epanomeritakis, Matthew Grennan, Joseph R. Martinez, Fiona Scott Morton, and Ashley T. Swanson

NBER Working Paper No. 34039

Over the last two decades, hospital systems and health insurers have acquired many types of providers, including physician practices, nursing home facilities, and home health agencies.

Past research has shown that horizontal mergers of both hospitals and physician practices–when one hospital buys another or two physician practices merge–push up the price of care and lead to local job losses.

Now, a new analysis of 276 hospital acquisitions of private practices is the first to show that vertical mergers also contribute to rising health care prices, and that these acquisitions increase both hospital and physician prices through anticompetitive mechanisms.

KEY LEARNINGS

- Hospital prices for labor and delivery increase by 3.3% ($475), and physician prices increase by 15.1% ($502) following integration.

- Price increases are driven by three anticompetitive mechanisms: foreclosure, recapture, and horizontal concentration effects.

- The mergers have reshaped the $1 trillion US physician industry, nearly doubling the share of physicians working for hospitals between 2008 and 2016.

- An estimated 99.9% of these transactions fell below Hart-Scott-Rodino reporting thresholds, meaning this massive industry transformation occurred with virtually no antitrust scrutiny.

Motivation

While theory suggests that non-horizontal mergers between complementary providers like hospitals and physicians should reduce costs by eliminating inefficiencies, there are also competing theories that such mergers could lessen competition and cause prices to increase.

In this paper, the researchers use new data and a combination of novel techniques to study the effects of physician-hospital mergers. The researchers introduce novel data to characterize the evolution of physician-hospital integration, combine these measures with detailed claims data to estimate the impact of mergers on prices (which, the researchers find, increase on average), and present new empirical evidence on the mechanisms through which integration leads to price increases.

A Novel Measure of Integration

Prior efforts to measure physician-hospital integration have been hampered by a lack of comprehensive data, with previous studies correctly identifying integration status approximately 55-60% of the time.

In this paper, the researchers develop a new approach using machine learning methods combined with comprehensive administrative data. The researchers combine multiple data sources including Medicare billing records, hospital surveys, physician directories, and SEC filings to create a training sample of 916 unique practice groups covering over 540,000 physician-years.

The researchers manually verify integration status using IRS filings, press releases, and practice websites, then train random forest algorithms to predict integration for virtually every physician in the US between 2008-2016. This machine learning approach achieves 97% accuracy.

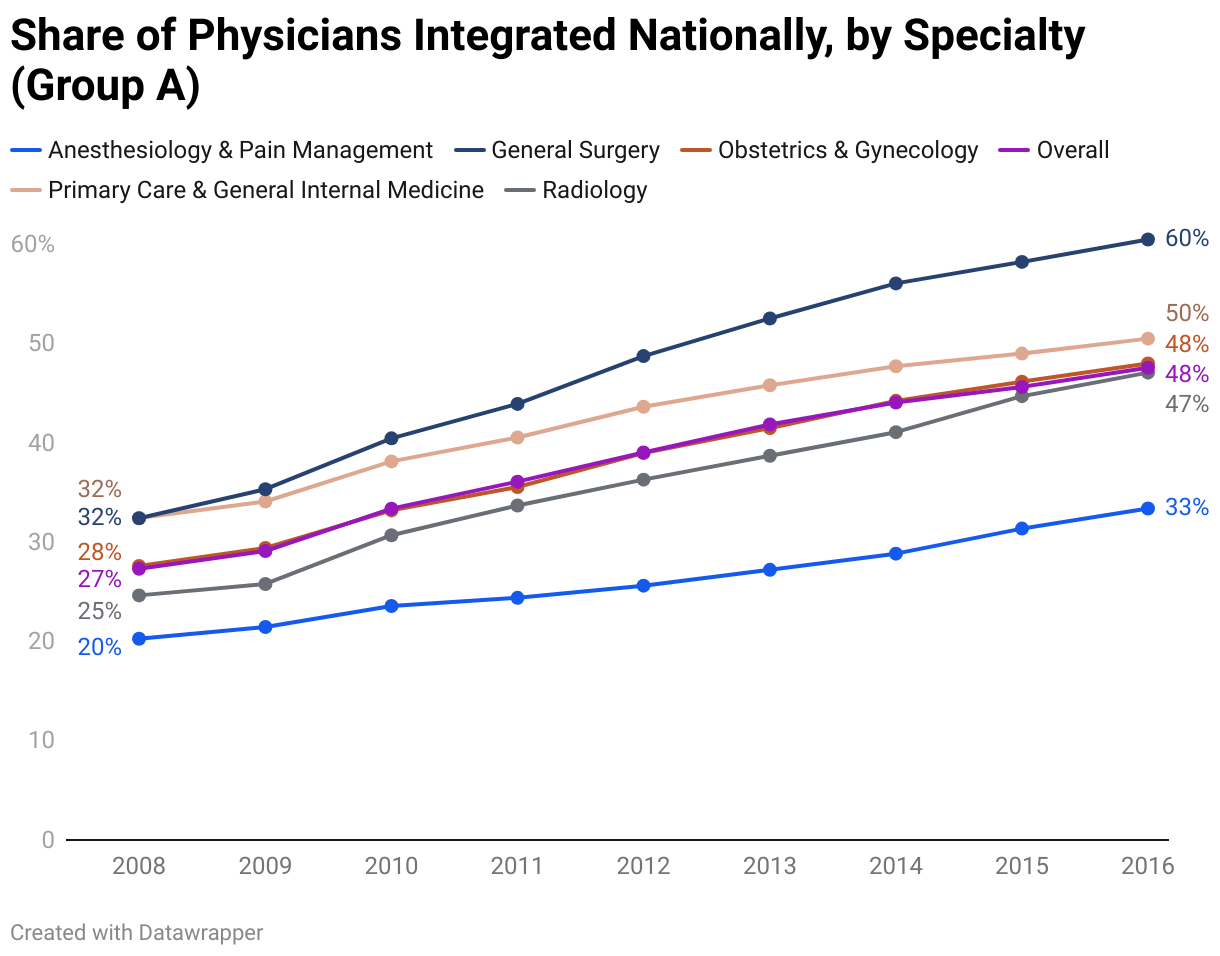

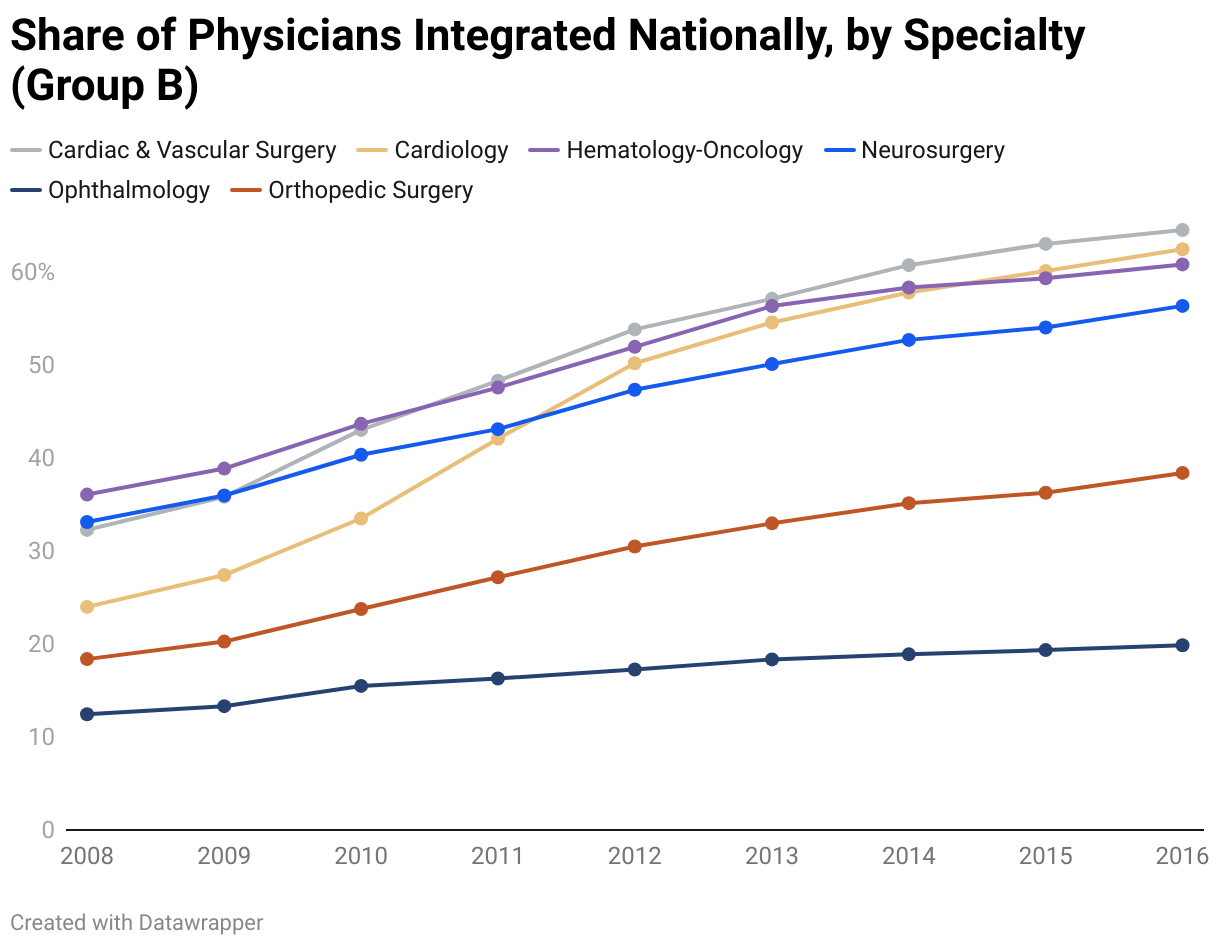

The data reveal that hospital ownership of physician practices increased 71.5% from 2008 to 2016, with nearly every region experiencing growth in integration. Among obstetricians-gynecologists, integration grew by 20.4 percentage points to 48% by 2016.

Price Effects

The researchers combine their integration data with detailed claims from a major national insurer covering labor and delivery services, the most common privately insured hospital admission. They focus on integration events occurring in 2013-2014, which allows them to observe prices for at least two years before and two years after each merger within their 2011-2016 data period.

To isolate causal effects, they use event studies comparing treated providers (those experiencing integration) to carefully matched controls. The researchers analyze which providers are close substitutes for patients, then exclude potential control providers who might experience spillover effects from nearby mergers.

The researchers find that integration events generate substantial price increases across provider types. Hospital prices for labor and delivery increase by 3.3% ($475) two years after integration, while physician prices rise by 15.1% ($502) following integration with hospital systems. These price increases substantially exceed what would be expected from efficiency improvements and represent significant cost increases to patients and insurers.

The researchers also find evidence that price increases are driven by anticompetitive rather than efficiency effects. Already-integrated physicians experience 9% price increases when their hospitals acquire additional physicians. Since these physicians' integration status remained unchanged, sudden quality or efficiency improvements cannot explain these price increases.

Anticompetitive Mechanisms

To explain why non-horizontal mergers between complementary providers increase rather than decrease prices, the researchers test three anticompetitive mechanisms through which physician-hospital integration can harm competition: foreclosure, in which acquired physicians concentrate their patients and services with the acquiring hospital system; recapture, in which integration with a highly-valued hospital followed by joint negotiation with insurers improves the physician's bargaining position; and horizontal concentration effects, where hospitals acquire multiple physician practices to increase market power.

Their empirical results provide strong evidence for each anticompetitive mechanism. Foreclosure generates larger price increases when acquired physicians shift patient referrals—hospital integration events with positive "steerage potential" produce 7.1% price increases compared to 1.7% for mergers without such potential. Recapture effects increase with acquiring hospital market power—physicians acquired by hospitals with high pre-merger willingness-to-pay experience 24.1% price increases versus only 5.6% for those acquired by low-market-power hospitals. Horizontal concentration amplifies price effects through physician market consolidation—when hospital acquisitions increase local physician market concentration significantly, integrating physicians experience 23.1% price increases compared to 8.6% when concentration remains unchanged.

Policy Implications

The researchers conclude that many of the observed mergers are likely anticompetitive and harm both consumers and end payers of health care services by increasing the cost of care without generating commensurate increases in quality.

The scale of this integration wave and its competitive effects reveal a significant enforcement gap in antitrust policy. From 2008 to 2016, the share of physicians working for hospitals increased 71.5%, while federal enforcement agencies challenged virtually no physician-hospital transactions. This means that an enormous sector of the US economy—approximately 6% of GDP—was reshaped without substantial antitrust scrutiny.

Despite the strong evidence that physician-hospital mergers raised prices, the researchers flag that they are aware of only a handful of federal investigations of these types of transactions. Likewise, there has been little enforcement by state attorneys general under the competition statutes of their states. This is particularly unfortunate, they write, because physician-hospital transactions are arguably too small to be handled efficiently at the federal level. Their results suggest that antitrust enforcement agencies trying to preserve competition in health care markets and keep prices from rising should take action against many physician-hospital mergers.

The results also provide guidance on observable pre-merger characteristics of transactions that tend to lead to the largest price increases. Deals with the most potential to increase either foreclosure (where the acquired physicians are most likely to shift their referral patterns) or recapture (where one of the merging parties already commands significant market power) generate the largest price increases.